Housing obsession

By Nick Chapman, independent NSW candidate for the Australian Senate.

Expensive Housing

Housing in Australia is expensive. Sydney was recently ranked in January by Demographia as the 2nd most expensive in the world, in relation to income.

Expensive housing is not just a financial issue, it is also a social issue. Young people and the less well-off are struggling to buy a home and homeowners are spending huge amounts of money on mortgages. Australia’s outsized housing market diverts investor money away from other areas. Huge mortgages also pressures people to prioritise earning money over their family and social life.

I believe the current trajectory of housing affordability will entrench a wealth gap between poor and rich, and young and old.

One of the drivers of increasing home prices are the generous tax incentives available to investors – particularly negative gearing and the Capital Gains Tax (CGT) discount.

I will explain these two incentives and my proposal for housing investment to make them fairer. Just to be clear, these proposals are specifically for housing investment.

Negative Gearing

Negative gearing essentially allows investors to make a loss and claim a tax deduction for this loss against their income tax. If expenses such as loan interest exceed rental income, the difference can be used to reduce income tax paid. It is available for various investments, including shares, but is most commonly associated with housing investment.

This is particularly beneficial for high-income earners as it reduces their tax. It was once ‘spruiked’ to me by an accountant as only worthwhile if you earn over $80,000.

Warning, we will start to get a somewhat technical here!

Capital Gains Tax

But it is the combination with the CGT discount where investors really benefit.

If you sell the home you live in you pay no CGT, ie, the profit is tax-free. I support this.

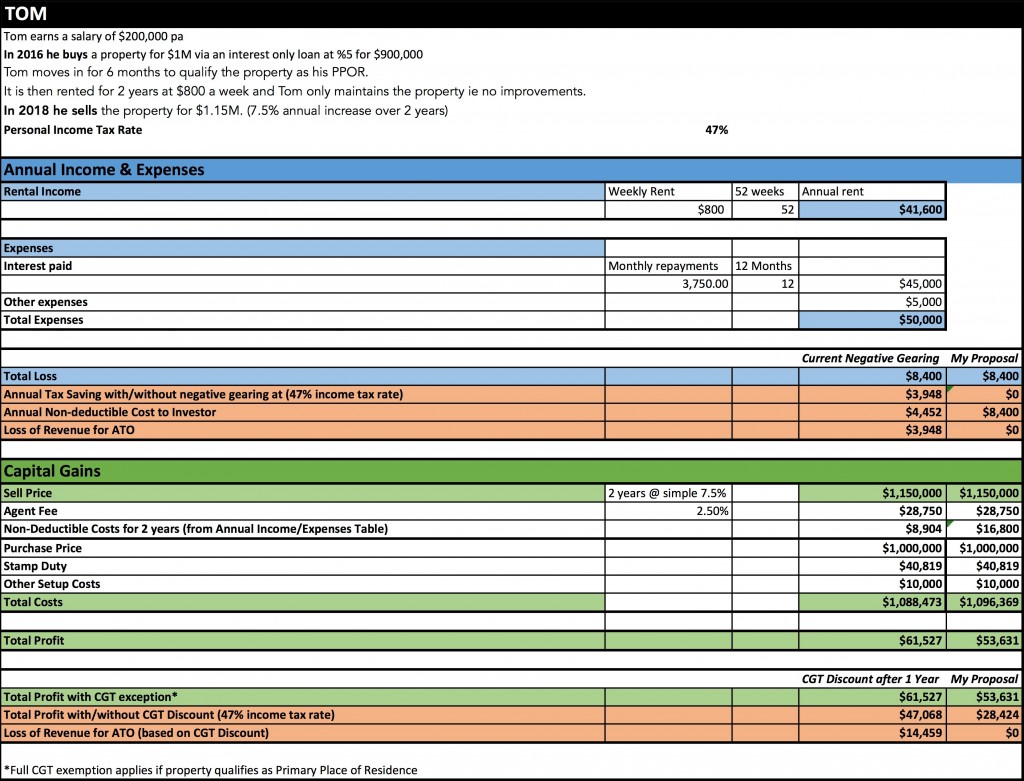

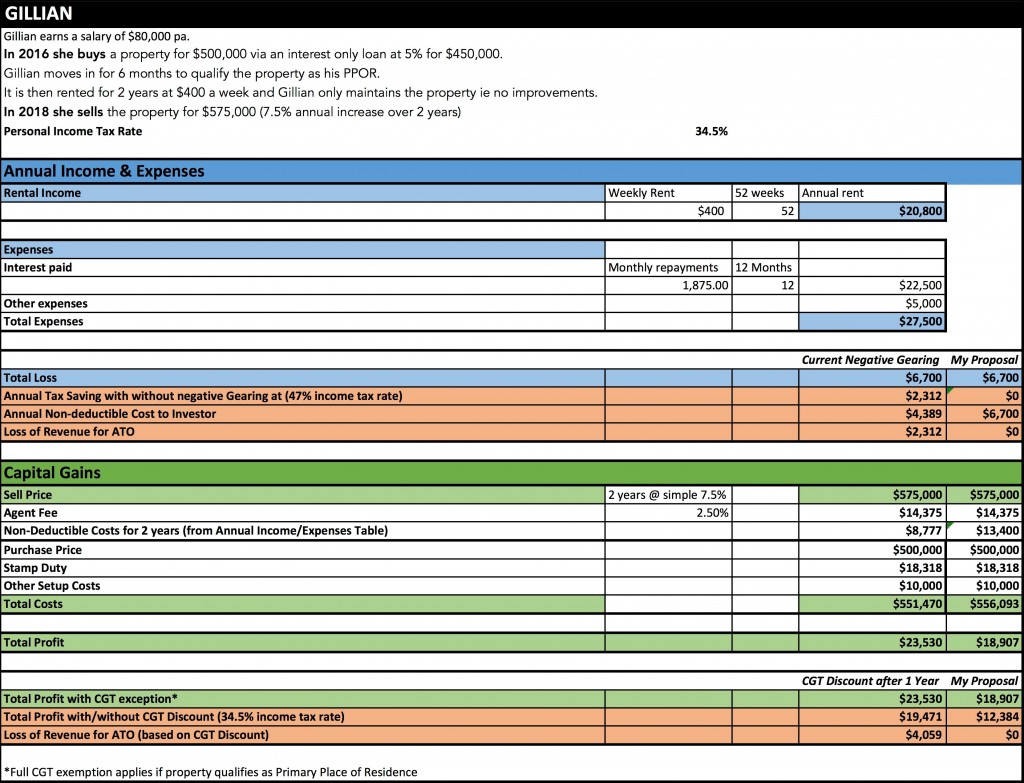

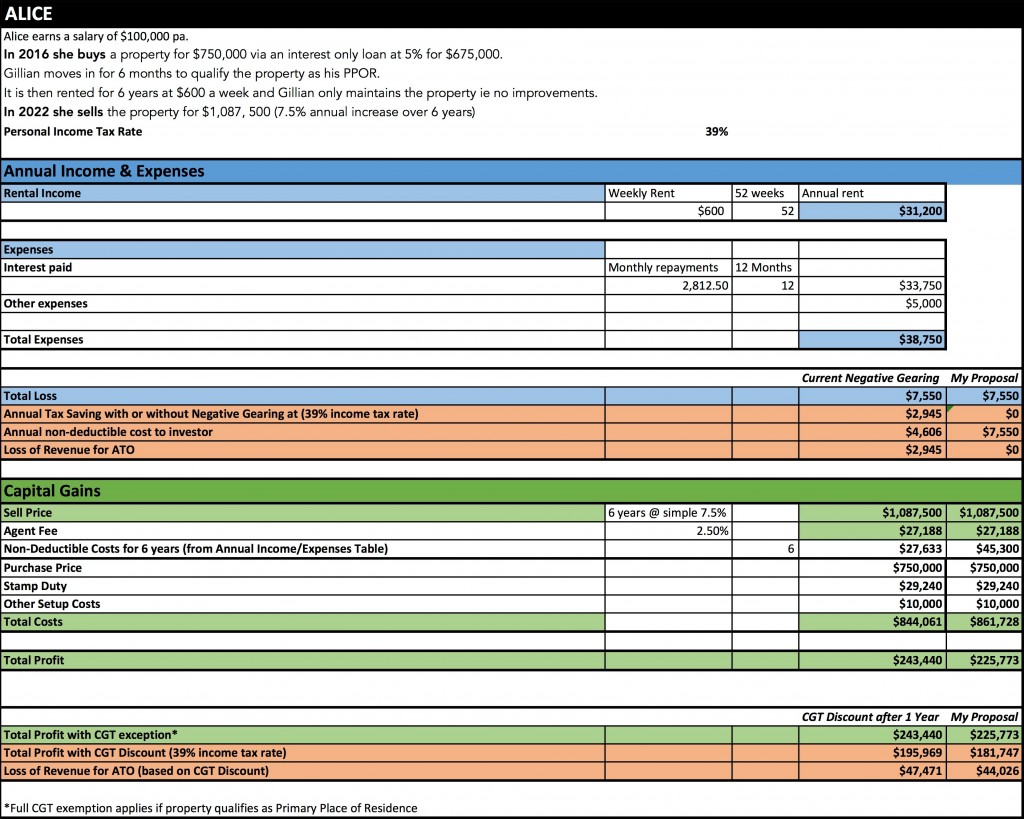

However, CGT is due (at your income rate) for investment profits. But you pay only half the rate if you hold the investment for more than 12 months. So for a high-income earner you would pay 24.5% tax on your investment property rather than 47%.

And there are even ways to get around the CGT altogether for investors.

When an investor buys a property they can move into it immediately for 6 months, qualifying it as their Principal Place of Residence (PPOR). They can then rent it out for another 6 years and sell it for a profit and pay no CGT. The ATO does have eligibility rules for this – there is also plenty of free and paid advice on how to qualify for those rules.

Ultimately, the combination of these two tax incentives results in speculative investment in property. The significant tax savings, especially to high-income earners, means property is invested in like growth shares – there is little intention of making a positive yield, ie, making an ongoing profit from rent, only a bet on values increasing in the future.

This drives up prices in a distorted manner that is not linked to wage growth, making it harder for non-investors to afford property.

Taxpayers are also indirectly funding investors through these tax incentives.

While negative gearing deserves scrutiny, I think the CGT discount is where the big dollars are.

My proposals in this area are as follows:

CGT Discount Proposal

The waiting period for CGT discount for property should be extended from the current 1 year to somewhere between 3 and 5 years.

I believe a discount is warranted to encourage people to invest and take risk, and to deal with inflation. However, 12 months is too short a time-frame, encouraging short-term speculation which drives prices up.

This would be implemented gradually by extending the waiting period by one year annually until we reached the desired waiting period.

Following the waiting period being extended and the impact to the housing market assessed, we should also consider reducing the discount from 50% to 25% over a 3 year period.

Principal Place of Residence Loophole

The ability to have a home classed as your place of residence when you don’t live in it needs to be tightened up or possibly abolished. You should not be allowed to make a tax-free profit on an investment property.

The current policy is open to exploitation and there is advice out there to help you.

Here’s some examples of advice from a Domain article: “You can live in your property, then let someone else live in the same property, but still claim it as your principal place of residence (PPOR) for up to six years” and “The obvious big plus is that if you own two properties, the one with the most capital gain can be claimed as your PPOR. Talk about a good idea!”

This needs to be addressed.

Neutral Gearing Proposal

According to the Australia Institute the only OECD countries that allow full deduction of interest payments are Australia, Japan, and New Zealand.

The deduction essentially allows property that makes a negative rental income to still be viewed as viable. Again, it encourages speculative investment for capital gain.

I propose that expenses, including interest, only be deducted against the investment income. Essentially, your investment loss claims would be quarantined to your investment, it could not be claimed against other income.

This would be neutral gearing rather than negative gearing.

This would be phased in over 4 years by dropping deductibility in excess of investment income 25% annually until it reaches 0%.

A phase in of this policy could avoid any dramatic impact to the property market, and also allow for interpretation of the effects of the policy.

Finally…

I suggest phased changes to avoid any sudden impact to the housing market. This phased approach would also help negate the need for “grandfathering” of current arrangements as is proposed by Labor. Grandfathering allows those investments benefitting from current arrangements to continue to do so indefinitely, while new investments would be made under the new rules. Grandfathering adds unnecessary complexity to the tax system and entrenches the wealth divide, particularly between young and old.

My proposal would help to reduce speculative demand in the property market and also increase federal tax revenue. It would help to reduce price growth in the property market giving the average person more chance of buying their own home and reduce our nations unhealthy obsession with property.

(The below 3 examples compares current incentives versus my proposal).

What are your thoughts on housing affordability?

About Nick Chapman: Nick is a consultant whose experience includes working in Canada and the UK. Nick values freedom, respect, integrity and innovation and believes in policies that benefit society as a whole. Nick stands for:

• A fair economy for a healthy society

• An independent check on government power

• Individual freedom and individual responsibility

• Political transparency

Find out more at www.nickchapman.org

15 comments

Login here Register here-

Garth

-

Backyard Bob

-

Carol Taylor

-

Nick Chapman

-

Backyard Bob

-

Matters Not

-

Garth

-

Matters Not

-

Matters Not

-

Terry2

-

David

-

townsvilleblog

-

Gangey1959

-

jimhaz

-

iggy648

Return to home pageThanks Nick for your proposals. Can I ask what are you a consultant for? Also, assuming you were elected to the senate under a Labor government, would you vote for their proposals even if any amendments you might table (in line with your above article) are rejected?

How about a Royal Commission into the Real Estate industry? Or, I dunno, any sort of investigation ….

I am pleased that someone is also tackling this issue. From my perspective, it seems that our current housing situation is a disaster for the future. We currently have far fewer young people able to start whittling away at a mortgage unto their mid 30s or older – due to a number of factors which includes the length of time needed to acquire qualifications, HECS debts to be paid for prior to starting to be able to save, insecure and often intermittent employment opportunities. This then leads to a far shorter time than say 20 years ago, to be able to pay off a mortgage..all in the mean while we have a government telling people of the necessity to save from an early age to be able to have a reasonable retirement. I would ask How? How can young people save, how to pay off HECS debts, how to pay off an extremely high mortgage and somehow still have money left over?

Hi Garth,

I’m a organisational change consultant.

My general approach to reviewing legislation

would be to negotiate for what I see as better outcomes.

Saying that, as a pragmatist I believe incremental improvement is better than no improvement.

So a direct answer! I believe Labor’s proposal needs improving but would support it over no action.

Thanks

Nick

Nick,

“I will:

Stand up against the growing nanny and police state (eg restriction on freedom, lockout laws)”

Expand, please.

the profit is tax-free. I support this Can you explain using economic concepts why you support an arrangement that ‘distorts’ not only the housing market but also affects and effects ‘investing’ across the broader market.

In short why should the 50X million dollar house I live in be disregarded when it comes to ‘pension’ consideration while my $250 000 dollar boat combined with my $100 000 residence disqualifies me from that same pension?

BTW, I really and truly love my boat and so do my children and grand children while all of us don’t really give a rats about the residence..

Just askin …

Or are some ‘assets’ deemed more worthy than others? If so, then what criteria are you employing. Please explain.

Thanks Nick. A direct answer is refreshing. Best of luck.

Nick here’s another example you may wish to consider. ‘A’ owns a personal residential house worth $100 million which he/she bequeaths to the offspring. No tax to be paid. (Time limits etc apply)

Or, on the other hand, ‘A’ has superannuation of $100 million which is also bequeathed to the offspring. Tax to be paid at 17.5%.

Notice how the ‘housing’ market might be distorted?

Sure does. Put your money into your house because the capital gains will be tax free. Extend, renovate, ‘add value’ and the like because the capital gain is all tax free. You’d be a mug to do otherwise. Just ask Malcolm why his house is so big. And valuable. (Acquired adjacent properties and the like).

Yep! In the same way as they are funding those who add value to their ‘family’ home.

Truth is, that if you allow a ‘tax rort’ then the smart punters will exploit same. And those who don’t want their home (their asset) to be free from taxation consideration will end up subsidising the already rich and powerful.

It is not ‘housing’ affordability that is the problem – buildings cost are a variable and builders are competing in the new housing market and right now is a very good time to be building a new house.

The problem is the availability of land in urban areas and as most undeveloped land is held by the state, we should be releasing substantial areas of land – not necessarily to developers – and ease the pressure on availability and prices.

We are entering a housing market growth cycle of 14 years. If interest rates remain low for the next 10-15 years, as forecast, then it is an ideal time to build or buy a house. Constructions costs are reducing, relatively, but the cost of land is increasing. By providing additional land for housing, the governments can help to contain the rate of cost increases for land. If projects like the inland rail link from Queensland to Victoria are funded, then land close to the rail links will be attractive. It would be refreshing to see some political statesmanship and leadership with vision to make this happen. I am not holding my breath, waiting for such actions.

I feel very sad for young couples today looking to purchase a home of their own. When I purchased my home in 1984 a high set home with no frills, it cost me $60,000, today it would sell for approximately $280,000 however before anyone thinks of moving to N.Q. they don’t build houses like mine anymore. Today it is just a slab of concrete on the ground, and blocks with a tile roof,(which is easier to construct, more profit) however these days the house comes with a lawn, lots of internal gizmo’s and the price is at least $350,000 It seems the buyers no longer want to buy the cheaper version and gradually add their own lawn and gizmo’s they want it all “now.” They are of course hamstrung with a huge mortgage for most of their lives, whereas I paid mine off at age 42. The builders are the winners with the new homes. As for Sydney being so expensive, the day I visited Sydney I could see what I was breathing, the pollution was so bad, I certainly wouldn’t want to live there and I’m buggered if I know how the Real Estate’s keep the prices so high when Australia is such a huge continent and there are plenty of other great places to live?

It seems to me that we have a guy with a brain, and someone who has put some thought into something. If there are a few bugs to be ironed out, so be it.

Good luck Nick. Go for it.

I like these proposals as a casual observation. I did not spot anything lopsided.

If presenting this to the public I’d include the economic negatives of high house pricing in Australia. Housing inflation creates profits at the micro level but losses to the economy at the macro level – 1 trillion in borrowing from OS, opportunity cost of investment in non-productive capital compared to the same money being invested in productive industries etc.

“The ratio of household debt to disposable income has almost tripled since 1988, from 64 per cent to 185 per cent” (http://www.natsem.canberra.edu.au/storage/AMP.NATSEM%20Report_Buy%20now%20pay%20later_Household%20debt%20in%20Australia_FINAL.pdf) There are vast amounts of money locked up in mortgages, which people could be spending on stuff to boost the flow of money through the economy, and create jobs and growth. The banks,of course, are laughing all the way to the bank.